Loan Origination System(LOS) Web Application

User research | UX Design | Interaction Design

What is LOS (Loan Origination System)?

A loan origination system (LOS) is software that helps financial institutions which handles from generating leads till disbursement of loans to customer.

Problem Statement.

The Loan Origination System (LOS), initially developed by non-designers, was hindered by several manual processes due to the lack of design involvement at its inception. Sales, credit, and operations teams relied on inefficient workflows.

For instance, sales teams used emails for the approvals, credit managers manually underwrote in Excel sheets, and loan application allocations were tracked using Jira and spreadsheets. Credit managers had to manually search through 8 to 10 Excel sheets to find existing customers, which was time-consuming and prone to error.

Solution

I automated approvals, loan eligibility preparation, loan case allocation, customer search, vendor tracking, and integrated external websites like CERSAI. These improvements streamlined operations, reduced manual effort, and improved turnaround times.

Impact

Eliminated Jira for case allocation. Reduced 70% of the Eligibility finding process through automation. Saved 2 hours per case by automating the approval process and cut month-end reporting from 4 days to 1 click. Automated customer search saved nearly 14 lakh INR annually and reallocated 7 resources. CERSAI integration reduced registration time from 40 to 2 minutes.

"I played the role of a Product Designer in this project, conducting usability evaluations, primary and secondary research, and stakeholder interviews to align the LOS application with business goals. I designed the UX, validated it through usability testing, prioritized features, secured stakeholder buy-in for key processes, and delivered implementation-ready screens to the development team"

Design Process

01- Usability Evaluation

To identify key usability issues, I conducted a "Expert Review" of the LOS interface. Each screen was thoroughly analyzed to highlight what could be the pain points, inconsistencies, and areas for improvement.

This method also includes a few heuristic review.

The image on the right shows the original site map, which I created to assess the existing navigation structure. During this process, I identified a few redundant and unnecessary pages that complicated the user journey, presenting an opportunity to streamline the system for better efficiency and usability.

I used the Usability Quotient (UQ) framework by HFI (Human Factors International) to systematically assess the overall usability of the application.

The checklist-based approach ensured that all critical usability aspects were thoroughly reviewed. Involving three evaluators, including myself, helped minimize individual biases and provided a more balanced evaluation.

Our assessment yielded an average usability score of 19. Ideally, a good usability score should fall between 65 and 70. A score below 40 indicates a need for significant redesign

I presented the usability evaluation report to the product head and other stakeholders and we justified to gain their buy-in for conducting user research and validating the findings.

The UQ checklist helped me track the usability score over time. By April 2023, the UQ value had reached 45; as of October 2024, it surpassed 50.

02- Research

After the usability evaluation, it became clear that a deeper understanding of existing processes, team structures, user goals, pain points, and tasks was essential. To achieve this, I secured buy-in from the product head during the usability evaluation report walkthrough to conduct primary research.

Research Objective

-

Identify all teams involved in the loan processing journey.

-

Classify users as primary, secondary, and tertiary based on product usage and interdependencies.

-

Study users' goals, tasks, pain points, expectations, and their working environments.

-

Understand current process flows, loan products, and interfaces users rely on.

-

Assess how efficiently users achieve their goals.

-

Validate usability issues identified during the evaluation process.

Inspired by the parable of the "Blind Men and the Elephant," it was essential to understand the entire ecosystem. The product was complex, with diverse users, interdependencies, and multiple loan products, requiring thorough research to gain a holistic view.

If I didn't achieve a holistic view, I would have risked addressing only isolated issues, leading to fragmented solutions that could create inefficiencies, missed opportunities, and conflicting workflows. This would undermine the user experience, slow down processes, and hinder the product's overall effectiveness.

Hand Drawing By Vidya

Before engaging with users, I conducted secondary research to prepare thoroughly for the primary research phase:

-

Explored the organization's structure through internal flowcharts and hierarchy systems.

-

Consulted with product managers and developers to understand the loan products, users, teams, roles, and various stages within the LOS.

-

Collaborated with HR to determine the headcount of each potential user team.

-

Identified the geographical locations of users across India.

-

Analyzed job descriptions from job portals to estimate sensitive data like role-specific salary ranges, ensuring confidentiality without directly asking users or HR.

-

Studied the ecosystems and processes of other companies in the lending business to gain additional insights.

2.1 Secondary Research

Job Descriptions from Naukri.com portal to understand the roles and responsibilities of the roles

Sales Manager, CPA, Credit Manager and Operation Executives

Secondary Research Findings

Image is blurred due to purposefully.

Discovered Sales Credit team, Operation team.

involved directly and potentially in loan application processing. And their responsibilities and task

I studied the LOS product ecosystem, its dependencies on interfaces, stakeholders, users, end customers, and DSAs, along with their interconnected environments.

Secondary Research Key Findings

Information is collected from different resources likeOrganisation hierarchy charts.HR InductionTechnical team to know about user’s headcountJob portal to understand user’s sensitive information like salary. And also high level understanding on their roles and responsibilities.

-

User Roles and Responsibilities: Gained a high level understanding of the tasks, responsibilities, and dependencies between sales, credit, and operations teams.

-

Educational Background and Salary Range: Identified the general educational qualifications and approximate salary ranges for key user roles.

-

Geographical Presence: Mapped the distribution of users across India to plan effective research outreach.

-

Stakeholder Identification: Identified key product and business stakeholders critical for aligning design solutions.

-

Lead Generation: Discovered that sales generate leads through multiple channels, including an extensive DSA (Direct Selling Agent) network.

-

Multiple Interfaces and User Behavior: Found that users relied on multiple tools—such as LOS, LeadSquared, and LMS—for various tasks. Sales teams were using the LeadSquared portal to punch in applications and upload documents, a task originally intended for DSAs.

Insight: DSAs were reluctant to perform these tasks, leading to sales managers taking over their work. This user behavior suggests that, if properly understood earlier, the LeadSquared portal might not have been needed, or its purpose could have been more effectively defined.

A few documents about the user list were collected from HR.

Team's and user's heirachy structure studied from organization's internal portal.

2.2 Primary Research

Research Planning

Research Execution

28

Total User Interviews

22

06

As Facilitator

As Observer

Location 1: Delhi (India) Office

- Credit Team

- Interacted with different roles within the credit team. And also learnt how team is also distributed for different loan products.

Location 2: Banglore (India) Office

- Operation Team

- Other teams Like Fraud Detection In Loan applications & Customer Experience Team

Location 3: Remote Interviews (Other Parts Of India)

- Sales and Other Teams.

LOS Ecosystem Map

The research helped me map out the ecosystem and gain an overview of all the information gathered. Mapping the entire ecosystem was essential to understanding the teams, their interconnections, and their dependencies.

Interconnected teams and their dependencies. Identified overlaps and redundancies in understanding dependencies and interconnections help in anticipating and mitigating potential risks. Aligned Goals: Helps align team objectives with the overall platform goals, promoting a unified direction.Clear Communication Channels: It clarifies communication paths, ensuring effective information flow.Provides a foundation for strategic planning for further redesigning.

Primary Research Key Insights:

-

Inconsistent Communication System: The sales, credit, and operations teams lacked a structured communication process, leading to uncoordinated interactions within and between teams.

-

Discrepancy Management Issues: Each team tracked and communicated discrepancies in their own way. The CPA (Credit Team) raised discrepancy queries through Jira, while the sales and operations teams managed them using master spreadsheets for different loan products.

-

Inefficient Document Management System: All three teams found the document management system on the LOS platform user-unfriendly due to the lack of bulk upload and download options. The sales team often uploaded the same applicant’s documents twice because of a broken flow between the LOS and another punching platform. Additionally, applicants had to sign over 50 pages for business loan products, frustrating both sales managers and applicants.

-

Broken Workflows and Manual Processes: Teams relied on tools like Jira, emails, and spreadsheets to manage loan applications, seek approvals, and track statuses. These disconnected workflows made the process cumbersome.

-

Repetitive Tasks: Teams performed many repetitive tasks. For example, if a loan application was rejected, they had to re-enter the applicant’s data and re-upload documents. The "Comment" feature on the LOS platform was used inconsistently, with only a few roles utilizing it. This forced teams to duplicate information in spreadsheets, as others did not rely on the LOS comments for communication.

2.3 Stakeholder Interviews

To understand the business goals and stakeholder vision, I spoke to product heads, managers, CTO, technical stakeholders, and other Stakeholders. Stakeholder shared their vision and current state of LOS (In 2023) along with business golas.

Thematic Analysis of Stakeholder Interviews Notes

Themes Emerged from the notes

Insights From Thematic Analysis

1. Automation:

-

Automating loan application allocation and underwriting increases efficiency.

-

Automated approvals improve communication between teams, resulting in faster turnaround times (TAT) and reduced human dependency.

2. Cost Effectiveness:

-

Reducing costs associated with field agents, fraud control agents, CIBIL pulls, and Sherlock services.

-

A focus on increasing the number of back-office employees to support digital processes over field operations.

3. Analysis:

-

Monitoring TAT helps identify bottlenecks—understanding which team or dependency causes delays.

-

Insights from tracking tools and dependencies help in optimizing the loan approval process.

4. Increase in Revenue

-

Opportunities to cross-sell additional services (e.g., insurance, provident fund).

-

Providing value-added services like bank statement analysis to attract more customers and improve business outcomes.

-

Generating green cases (approved loans) to maximize revenue.

5. Data on System

-

Ensuring the availability of complete customer data throughout the loan lifecycle (before and after disbursement).

-

Keeping a system of records and audit trails to ensure compliance (e.g., audits by RBI).

6. Efficiency and Smart Workflows.

-

Reducing workload by minimizing repetitive tasks and improving processes.

-

Reducing TAT through optimized workflows and adoption of loan products aligned with customer needs.

-

Addressing system glitches, load times, and data pull issues to ensure smooth functioning.

7. Unified Tool.

-

Reducing dependency on external tools (e.g., LeadSquared) by building integrated solutions in the LOS platform.

8. Insights for Reporting and Optimization.

-

Consolidating metrics on approvals, rejections, and loan volumes for real-time tracking and decision-making.

-

Analyzing trends and post-facto data to improve future processes and productivity.

-

Sampling data and monitoring team performance to identify areas of improvement.

Business Goals

1. Automation: Streamline loan processing with automated allocation, underwriting, approvals, and tracking

2. Cost Reduction: Cut expenses on field agents, fraud control, CIBIL pulls, and third-party services.

3. Analytics: Monitor TAT, identify bottlenecks, and improve process efficiency.

4. Increase Revenue: Boost cross-selling (insurance, PF) and increase approval of quality loan cases.

5. Unified Data: Ensure complete data availability and maintain audit records.

6. Efficiency: Reduce TAT, eliminate redundant tasks, and resolve technical issues.

7. Integrated Tools: Replace external tools with a unified platform to streamline workflows.

03- Personas

Role Based Persona creation approach is adopted to create persona because initially LOS had wide set of roles who were the potentially using the LOS product. Post automating the workflows and removing the manual processes the persona reduced.

Persona Before Research

Current (2024) Personas

Projected Personas

1.Sales Manager

2.CPA Login

3.CPA CAM

4.Credit Manager

5.Operation Manager

1.Sales Manager

2.CPA

3.Credit Manager

4.Operation Manager

1.Sales Manager

2.Credit Manager

3.Operation Manager

04- Process & Task Flow Evaluation

05- Product Design Strategy

Feature list and it's prioritization using KONO model.

Designing for multiple personals & multiple loan products

Design Strategy

Collaborated with cross-functional teams like

1. Product Stakeholders

2. Business Stakeholders

3. Development Team.

4 . Users.

To form a "Design Strategy"

This method is From HFI's CUA Certification.

06- Featurewise Designs

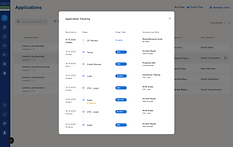

Feature 1: Auto Allocation

Auto allocation is auto assigning of "Loan Application" to each role using round robbin

Pain Point: Users used use Jira to check their assigned loan application to be processed.

Research:

Solution Diagram

.png)

Wireframes

Visual Designs

Usability Testing

Designs Before and After Comparison

Before

After

Future Phase Enhancements kept aware to product and dev team

Scenario Comparison